Conformalized Forecasting using Machine Learning (and statistical) models with ARCH effects

mlarchf.RdConformalized Forecasting using Machine Learning (and statistical) models with ARCH effects

mlarchf(

y,

h = 10L,

mean_model = forecast::auto.arima,

model_residuals = forecast::meanf,

fit_func = ahead::ridge,

predict_func = predict,

conformal = FALSE,

lags_vol = 10L,

type_pi = c("surrogate", "bootstrap", "kde"),

type_sim_conformalize = c("surrogate", "block-bootstrap", "bootstrap", "kde",

"fitdistr"),

ml_method = NULL,

level = 95,

B = 250L,

ml = TRUE,

stat_model = NULL,

n_clusters = 0,

clustering_dist = "euclidean",

clustering_method = "kmeans",

...

)Arguments

- y

A numeric vector or time series of class

ts- h

Forecasting horizon

- mean_model

Function to fit the mean model (default:

forecast::auto.arima)- model_residuals

Function to model the residuals (default:

forecast::thetaf)- fit_func

Fitting function for the variance model (default:

ahead::ridge)- predict_func

Prediction function for the variance model (default:

predict)- conformal

A boolean; either use conformal prediction or not

- lags_vol

Number of lags for squared residuals regression

- type_pi

Type of prediction interval ("kde", "surrogate", or "bootstrap") for volatility modeling

- type_sim_conformalize

Type of simulation for conformalization of standardized residuals ("block-bootstrap", "surrogate", "kde", "bootstrap", or "fitdistr")

- ml_method

caret package Machine learning method to use, if

fit_funcandpredict_funcaren't provided. If NULL, usesfit_funcandpredict_func. Seeunique(caret::modelLookup()$model).- level

Confidence level for prediction intervals

- B

Number of bootstrap replications or simulations

- ml

If

TRUE,fit_funcandpredict_funcare used, otherwise a statistical model instat_model- stat_model

A statistical model, e.g

forecast::thetaforforecast::auto.arima- n_clusters

Number of clusters for residuals (default is 0) for

ml == TRUEandml_methodnotNULL- clustering_dist

Only if

n_clusters > 0. If "euclidean", then mean square error, if "manhattan ", the mean absolute error is used.- clustering_method

Only if

n_clusters > 0. If "kmeans", then we have the kmeans clustering method, if "hardcl" we have the On-line Update (Hard Competitive learning) method, and if "neuralgas", we have the Neural Gas (Soft Competitive learning) method. Abbreviations of the method names are accepted.- ...

Additional parameters to be passed to

stat_model

Value

A forecast object containing predictions and prediction intervals

Examples

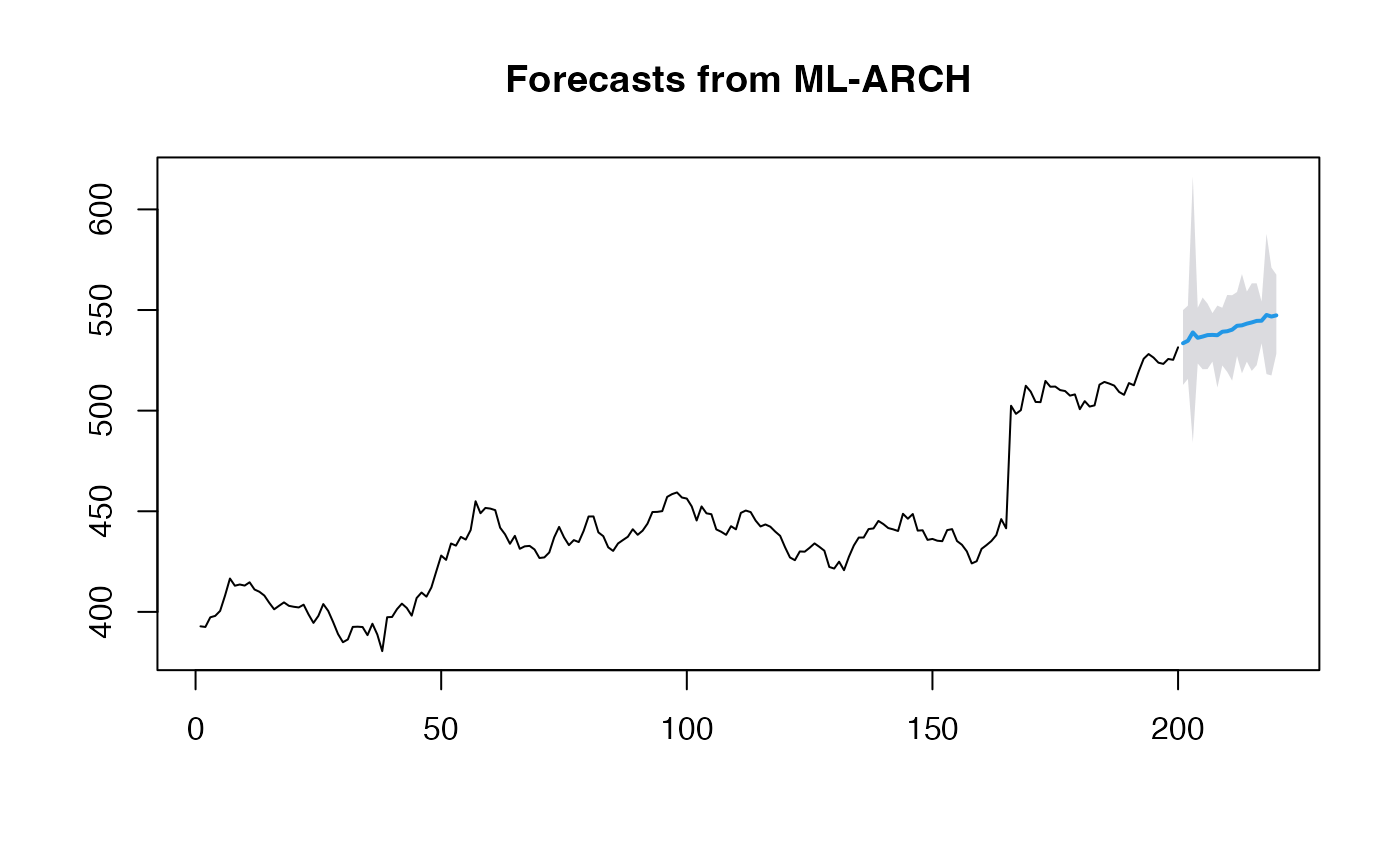

y <- fpp2::goog200

par(mfrow=c(2, 2))

(obj_ridge <- ahead::mlarchf(y, h=20L, B=500L, conformal=TRUE))

#> Point Forecast Lo 95 Hi 95

#> 201 534.4214 513.0126 549.3934

#> 202 536.2434 516.2732 554.8151

#> 203 536.4303 521.4627 553.5272

#> 204 536.6375 516.4953 559.5297

#> 205 536.9744 513.3215 555.6089

#> 206 536.8669 518.1739 552.4976

#> 207 539.0674 519.1329 558.1133

#> 208 537.4618 501.6435 560.6395

#> 209 540.1076 518.9179 558.1104

#> 210 536.5789 509.1344 555.3093

#> 211 540.7064 517.4373 555.1692

#> 212 543.6837 528.5274 561.0368

#> 213 543.4614 524.3126 564.4024

#> 214 544.3046 526.8850 564.2638

#> 215 544.1797 522.0492 560.9355

#> 216 544.7224 525.9826 560.9315

#> 217 545.7186 524.2705 564.2967

#> 218 546.5558 524.4958 568.5002

#> 219 546.0634 527.0138 562.9882

#> 220 548.5014 525.1078 567.3898

plot(obj_ridge)

print(mean(obj_ridge$upper - obj_ridge$lower))

#> [1] 39.69045

(obj_ridge <- ahead::mlarchf(y, h=20L, B=500L, conformal=FALSE))

#> Point Forecast Lo 95 Hi 95

#> 201 532.2466 517.5339 549.7756

#> 202 531.7224 508.7408 551.2735

#> 203 533.2419 519.0815 549.6869

#> 204 538.2220 519.6208 558.4489

#> 205 533.6841 515.4832 550.8369

#> 206 536.0713 522.1240 551.1259

#> 207 537.9695 520.3529 550.8776

#> 208 536.6699 519.0575 552.6136

#> 209 540.0722 520.8841 557.9272

#> 210 540.1827 527.2999 564.3716

#> 211 541.1687 524.6547 553.8595

#> 212 540.4668 524.1068 562.6405

#> 213 540.3615 522.8569 564.6440

#> 214 541.6808 524.9869 556.9404

#> 215 541.9843 526.4018 563.4523

#> 216 542.8743 527.5210 562.6983

#> 217 543.3401 528.7225 560.6608

#> 218 543.5208 522.6618 565.3813

#> 219 544.4165 528.6999 560.2330

#> 220 544.7700 526.8607 563.6331

plot(obj_ridge)

print(mean(obj_ridge$upper - obj_ridge$lower))

#> [1] 35.17146

(obj_ridge <- ahead::mlarchf(y, h=20L, B=500L, conformal=TRUE, stat_model=forecast::thetaf, ml = FALSE))

#> Point Forecast Lo 95 Hi 95

#> 201 538.0943 511.3731 599.5316

#> 202 532.7592 492.6637 561.5746

#> 203 535.6568 505.4333 574.0318

#> 204 536.4320 505.2108 562.3914

#> 205 538.5321 513.7271 572.9817

#> 206 538.4453 506.7213 584.0057

#> 207 538.5266 502.4655 572.0884

#> 208 540.0950 518.7978 568.7838

#> 209 539.1217 513.9889 573.2098

#> 210 540.4599 509.6873 566.7720

#> 211 542.2328 517.2629 579.0726

#> 212 542.7936 507.8171 581.9193

#> 213 542.4282 507.2424 582.2066

#> 214 546.1098 512.3549 595.3141

#> 215 544.6685 516.5238 597.2780

#> 216 541.0232 501.8039 573.0544

#> 217 540.6050 497.3601 577.0328

#> 218 545.2773 518.6021 581.7445

#> 219 546.9851 523.3497 586.1527

#> 220 547.9129 517.3082 577.3549

plot(obj_ridge)

print(mean(obj_ridge$upper - obj_ridge$lower))

#> [1] 68.34035

(obj_ridge <- ahead::mlarchf(y, h=20L, B=500L, conformal=FALSE, stat_model=forecast::thetaf, ml = FALSE))

#> Point Forecast Lo 95 Hi 95

#> 201 531.6567 514.0526 548.3243

#> 202 532.9804 511.2759 560.9922

#> 203 534.6671 518.1708 558.5576

#> 204 534.9105 511.9659 557.0808

#> 205 534.9256 518.7440 557.7363

#> 206 535.9355 518.3771 551.7302

#> 207 537.2476 520.0605 561.5851

#> 208 536.8801 518.2995 556.3820

#> 209 537.4439 520.6509 558.4829

#> 210 537.6221 522.2782 559.3128

#> 211 538.4523 522.5890 557.8461

#> 212 539.1346 523.1141 558.1896

#> 213 541.5791 518.9426 563.6007

#> 214 540.9385 521.0993 559.8572

#> 215 541.4986 521.7432 562.2131

#> 216 542.6545 527.2600 564.8567

#> 217 543.5398 525.5320 564.5464

#> 218 544.5900 527.8212 567.4387

#> 219 544.2469 523.9578 565.1556

#> 220 545.0149 525.0901 566.1182

plot(obj_ridge)

print(mean(obj_ridge$upper - obj_ridge$lower))

#> [1] 39.44909

par(mfrow=c(1, 1))

print(mean(obj_ridge$upper - obj_ridge$lower))

#> [1] 39.44909

par(mfrow=c(1, 1))